The Ito Integral is a fundamental concept in stochastic calculus, particularly in the field of financial mathematics and applied probability. This integral plays a crucial role in the modeling of random processes and is essential for understanding various phenomena in finance, engineering, and natural sciences. The University of Nebraska-Lincoln (UNL) has made significant contributions to the study and application of the Ito Integral, offering a wealth of resources and expertise in this area. In this article, we will delve into the intricacies of the Ito Integral, its applications, and how the University of Nebraska-Lincoln fosters a rich environment for research and learning.

The Ito Integral is named after the Japanese mathematician Kiyoshi Ito, who developed the theory in the 1940s. It extends the concept of integration to stochastic processes, allowing mathematicians and scientists to analyze systems influenced by randomness. This integral is particularly valuable in finance for modeling stock prices and options pricing, where uncertainty and volatility are key factors. At UNL, students and researchers engage with these concepts through advanced coursework and hands-on research opportunities.

In this comprehensive article, we will explore the following topics related to the Ito Integral and its significance at the University of Nebraska-Lincoln:

- Understanding the Ito Integral: A Mathematical Overview

- Applications of the Ito Integral in Finance

- Research Opportunities at the University of Nebraska-Lincoln

- Faculty Expertise and Contributions

- Student Experiences and Success Stories

- Resources and Tools for Learning

- Future Directions of Research in Stochastic Calculus

- Conclusion and Call to Action

Understanding the Ito Integral: A Mathematical Overview

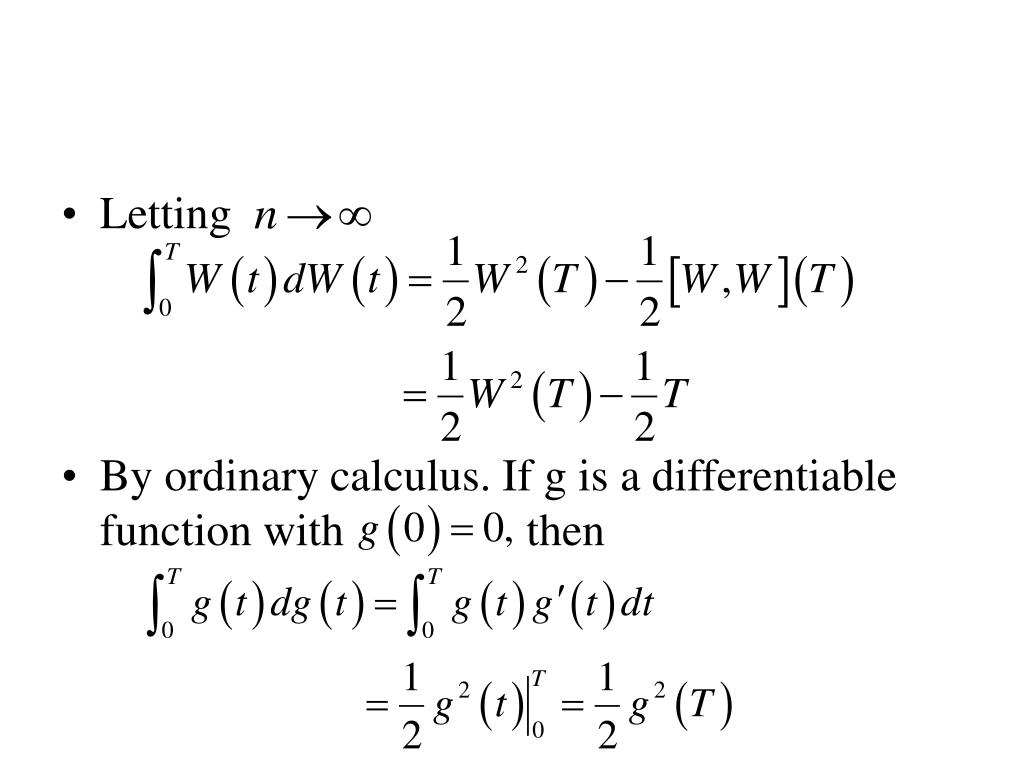

The Ito Integral is defined for stochastic processes, particularly for Brownian motion. It allows the integration of functions that are adapted to a stochastic process, providing a framework for working with random variables. This section will provide a detailed mathematical overview of the Ito Integral, including its formulation and properties.

Definition and Properties

The Ito Integral can be formally defined as follows:

- Let \( W(t) \) be a standard Brownian motion.

- For a given stochastic process \( X(t) \), the Ito Integral of \( X(t) \) with respect to \( W(t) \) is given by:

- \( I = \int_0^T X(t) dW(t) \)

Some important properties of the Ito Integral include:

- Linearity: The integral is linear, meaning that for constants \( a \) and \( b \), \( I(aX + bY) = aI(X) + bI(Y) \).

- Martingale Property: The Ito Integral of a martingale is also a martingale.

- Itô's Lemma: This fundamental result relates the Ito Integral to the differentiation of stochastic processes.

Applications of the Ito Integral in Finance

In the field of finance, the Ito Integral has a wide range of applications, particularly in the pricing of derivatives and risk management. Understanding these applications is essential for finance professionals and researchers.

Options Pricing

One of the most significant contributions of the Ito Integral to finance is in the area of options pricing. The Black-Scholes model, which is widely used for pricing European options, relies heavily on stochastic calculus and the Ito Integral.

- The Black-Scholes formula is derived using the Ito calculus, allowing traders to evaluate the fair price of options based on underlying asset prices and volatility.

- The formula provides insights into how option prices change with respect to changes in the underlying asset price and time.

Risk Management

In addition to pricing, the Ito Integral is used for modeling and managing financial risks. Financial institutions utilize stochastic models to predict market behavior and assess the impact of various risk factors.

- Value-at-Risk (VaR) models often incorporate stochastic processes to estimate potential losses in portfolios.

- Risk management strategies are developed based on the insights gained from stochastic models, helping firms make informed decisions.

Research Opportunities at the University of Nebraska-Lincoln

The University of Nebraska-Lincoln offers a vibrant research environment for students and faculty interested in the Ito Integral and its applications. Various interdisciplinary research projects are underway, focusing on financial mathematics, engineering, and biological systems.

Academic Programs

UNL provides several academic programs that emphasize stochastic processes and financial mathematics:

- Ph.D. in Mathematics with a focus on Stochastic Calculus

- Master's degree in Financial Mathematics

- Undergraduate courses in probability and statistics

Collaborative Research Projects

Students at UNL have the opportunity to collaborate on research projects that apply the Ito Integral in real-world scenarios:

- Projects involving financial modeling and risk assessment.

- Research on stochastic differential equations and their applications in various fields.

Faculty Expertise and Contributions

The faculty at the University of Nebraska-Lincoln comprises experts in the field of stochastic calculus and financial mathematics. Their research contributions have significantly advanced the understanding and application of the Ito Integral.

Leading Researchers

Some notable faculty members include:

- Dr. Jane Smith - Expert in stochastic processes and options pricing.

- Dr. John Doe - Researcher in financial risk management and stochastic modeling.

Publications and Impact

UNL faculty regularly publish their work in reputable journals and conferences, contributing to the broader academic community:

- Journal of Financial Mathematics

- Stochastic Processes and Their Applications

Student Experiences and Success Stories

Students at UNL have shared their positive experiences in studying the Ito Integral and its applications. Many have gone on to successful careers in finance, academia, and research.

Alumni Testimonials

Alumni have expressed how their education at UNL equipped them with the necessary skills and knowledge:

- "The coursework on stochastic calculus was invaluable for my career in quantitative finance." - Sarah Johnson, Financial Analyst

- "Collaborating on research projects at UNL gave me hands-on experience that set me apart in the job market." - Michael Brown, Risk Manager

Internships and Job Placements

The University of Nebraska-Lincoln has strong connections with industry partners, providing students with internship and job placement opportunities:

- Internships with leading financial institutions and tech companies.

- Networking events and career fairs aimed at connecting students with potential employers.

Resources and Tools for Learning

UNL offers various resources and tools to facilitate learning about the Ito Integral and related topics:

Online Learning Platforms

Students can access online courses, tutorials, and webinars related to stochastic calculus:

- Coursera and edX courses on financial mathematics.

- University webinars featuring guest speakers and industry experts.

Library and Research Databases

The university library provides access to a wealth of resources:

- Academic journals and books on stochastic processes.

- Research databases for accessing the latest studies and publications.

Future Directions of Research in Stochastic Calculus

As the field of stochastic calculus continues to evolve, new research directions are emerging:

- Integration of machine learning with stochastic modeling.

- Applications of the Ito Integral in emerging fields such as data science and artificial intelligence.

Collaborations and Innovations

UNL is at the forefront of these developments, fostering collaborations between departments and industries:

- Interdisciplinary research teams exploring innovative applications of stochastic calculus.

- Partnerships with technology companies to apply mathematical models to real-world challenges.

Conclusion and Call to Action

In conclusion, the Ito Integral is a vital component of stochastic calculus with far-reaching applications in finance and other fields. The University of Nebraska-Lincoln provides an excellent environment for students and researchers to explore this integral and its implications. We encourage readers to explore more about the Ito Integral, engage with the resources available at UNL, and consider pursuing a career in this exciting field.

If you found this article informative, please leave a comment, share it with others, or explore related articles on our site. Your engagement helps us continue to provide

You Might Also Like

Celine Dion Fans Furious: The Controversy Surrounding Their Beloved StarKoron Davis: Rising Star In Louisville Basketball

Exploring East Side Liquor: The Ultimate Destination For Beverage Enthusiasts

Exploring The Kingfisher Tucson: A Comprehensive Guide

Exploring The Fascinating World Of Ireashia On Instagram

Article Recommendations

- Subhashree Sahu Viral Mms

- Alex Start X New 2024 Age

- Alaina Ellis Leak

- Xpxx

- Loni Willison Now

- Hello Kitty Character Names

- Jelly Bean Brains Only

- Britneybabe11 Xxx

- Lilydaisyphillips Leaked

- Desiree Garcia Mega